Fintech is booming in Australia! The sector is now worth around $45billion AUS (over $30billion USD) – a 17900 per cent rise from 2015’s value ($250billion AUS/$168million USD) according to Fintech Australia. But what subsectors are leading the way and can the country keep up its growth?

First, let’s take a step back and look at the financial landscape in Australia more generally. Despite its market stalling in H1’24, Australia’s economy still remains a major player globally with a gross domestic product (GDP) per capita of over $65,000 according to the World Bank.

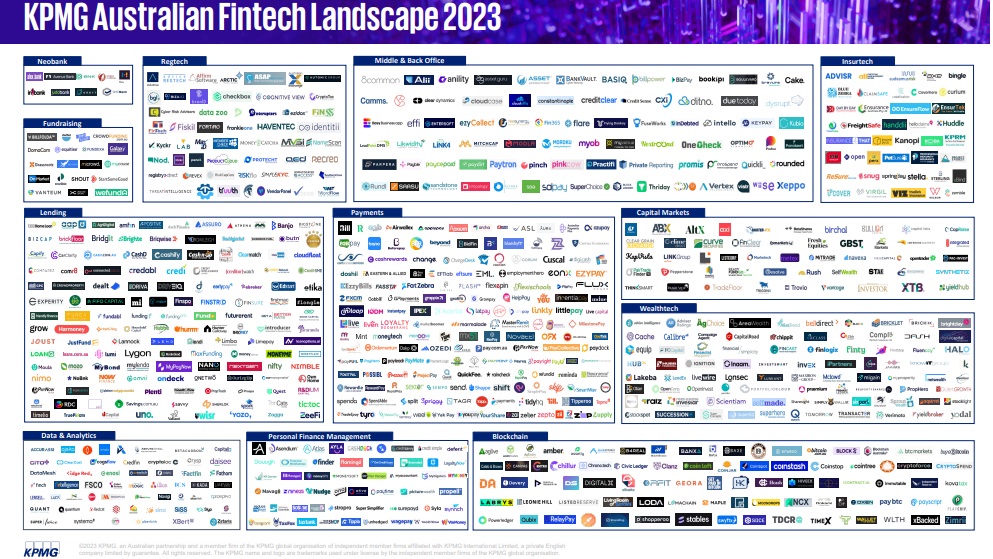

According to the KPMG Fintech Landscape 2023, the ecosystem is very diverse in Australia with over 830 independent fintechs headquartered in the region.

The fintech landscape

The Australian state of New South Wales, home to the country’s capital, has the largest percentage of fintech companies (60 per cent). This is followed by Victoria (24 per cent) and Queensland (12 per cent).

The country is also home to various unicorns. These include cross-border payments Airwallex, buy now pay later (BNPL) Afterpay and challenger bank Judo Capital.

The payments subsector is the largest in Australia. It has a 20 per cent share of all fintechs in the country with over 160 firms. Lending and wealthtech take second and third place respectively. Lending represents 17 per cent of the market (140 fintechs), while wealthtech represents 10 per cent.

Open banking is another notable subsector in Australia. The majority of the APAC region’s adoption of the technology has been market-driven – however, in Australia, regulations have driven its development. This was evident in July 2019, when Australia launched its open banking regime, based on consumer data right (CDR) legislation. The regime’s aim was to give customers more control over their data and easier access to products and services they required.

There were other milestones in 2019 too. For example, major banks celebrated application programming interfaces (APIs) and eligible product data, such as rates, fees, and terms and conditions. A year later, individual account holders and sole traders could share data relating to their retail banking products.

In 2021, data sharing was further improved as customers could share information business lending, trust accounts, overdrafts, asset finance, lines of credit and foreign currency accounts. Additionally, major banks allowed for data sharing for non-individuals, secondary users and business partnerships.

Recent news

Australia was not able to escape the declines in fintech funding experienced across the world. In terms of deal activity, it saw a 61.9 per cent decline from 42 deals in Q2’23 to 16 in QR’24. From a funding point of view, there was also a drop as the country raised $475million in Q2’24 which was 73.5 per cent lower than Q2’23 ($1.8billion).

According to Fintech Australia’s fourth edition of its Australian Open Banking Ecosystem Map and Report, which was supported by Mastercard, and in partnership with FinTech NZ, Payments NZ and Open Finance ANZ, the country saw a 165 per cent increase in consumer data right (CDR) participants. Other findings revealed that nearly all consumer bank accounts (99.74 per cent) are now connected to the open banking ecosystem, positioning Australia for further adoption of open banking technologies.

Last month, the Australian government proposed the introduction of a Scams Prevention Framework (SPF), implementing new mandatory scam obligations across all sectors. The Bill, which would insert the SPF into the ‘Competition and Consumer Act 2010,’ is expected to be introduced to the federal parliament next month.

The post Fintech’s Value in Australia Grows by 17,900% in Less Than a Decade appeared first on The Fintech Times.

{kind=link}