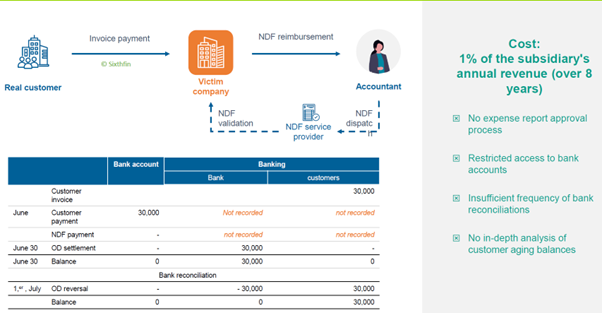

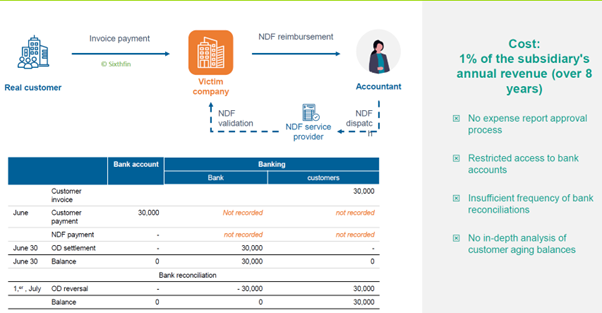

The cost of this fraud? 1% of the subsidiary’s annual turnover (over 8 years). It could have been halted before it got started by flagging bank deposits that do not have a corresponding accounting entry.

What is Invoices/Expenses Fraud & How Does it Work?

This type of invoice/expenses fraud is a structural risk that is often underestimated. The duration of exposure is as decisive as the unit amount embezzled, which in this instance was carried out over eight financial years and cost 1% of the subsidiary’s annual turnover. In this case, the mechanism was simple but invisible to the naked eye: a customer payment deposited in the bank was never recorded in the accounts, while a fictitious expense report, validated internally, reimbursed the same amount to the accountant.

In this case study we’re entering accounting mechanics. The subsidiary had a very small accounting team, and the chief accountant had the ability to process payments himself. The Group also used an external service provider to manage expense reports.

The issue with such providers is that their role is generally limited to checking that receipts exist. They don’t know the company’s internal rules, nor can they challenge the validity or appropriateness of the expenses submitted.

Eight years of fraudulent activity

Here’s what happened: several clients were paying their invoices normally, but these payments were not recorded in the accounting system. At the same time, the chief accountant was submitting expense reports, which were approved by the external provider. He then reimbursed himself using the funds received from clients’ payments that had never been booked. The amounts appeared on the bank statements but not in the accounts.

During each monthly close, adjusting entries were posted to artificially record the client payments, then reversed the following month. This allowed the fraud to keep rolling smoothly from one month to the next. And it went on for eight years.

Why wasn’t it detected sooner?

Fraud can rumble on for many months, if not years before it’s detected. Some of the issues in this

case were:

- There was no proper internal process to validate expense reports.

- Bank account access was extremely restricted, and the chief accountant could authorise payments himself.

- Bank reconciliations were performed very infrequently — and unsurprisingly, by the chief accountant himself.

- No independent review of the accounts receivable ledger was ever performed: not by controlling, not by internal control teams, not by internal audit.

- With all these weaknesses combined, the fraud mechanism could operate comfortably and remain unnoticed for many years.

What can organisations do to prevent this type of fraud?

One of the issues with this type of fraud is the length of time it can go on for. The company is being systematically weakened by poor processes; no expense report, restricted access to bank accounts and infrequent reconciliation. This can be caused by siloisation; the concentration of responsibility in one person. The opportunity for fraud is revealed and rationalisation follows because of a lack of oversight.

Two Ways to Prevent Invoice/Expenses Fraud:

- Improve validation processes with proper verification

At the heart of this fraud were two flawed manual processes: the recording of customer receipts, which was often delayed or handled inconsistently, and the validation of expense reports, which were approved by management without verification of supporting documents or reconciliation with other flows. By automating the monitoring of bank reconciliations and integrating specific controls on expense reports, the organisation could have closed both of these windows of opportunity simultaneously. - Making fraud untenable through traceability and transparency

For eight years, the chief accountant was able to maintain this fraud because he was the only one with a complete view of the flows. To avoid this, organisations can use advanced technical solutions to redistribute visibility via a fully collaborative platform. In this environment, recurring monthly closing manipulations would be immediately flagged as points of attention, such as over-the-counter reversals on the 1st of the month to hide cash receipts.

How to Spot and Prevent Invoice/Expenses Fraud

- Monitoring reversal patterns and closing manual adjustments

Improve analyses of the recurrence and logic of various manual adjustments. A systematic reversal on the 1st of the following month, applied to the same amounts and the same accounts, may constitute an accounting anomaly that a platform immediately flags as a priority alert. This type of monthly closing manipulation should be one of the indicators covered by the organisation’s controls. - Cross-checks on expense reports Organisations can build customised control programmes for expense reports. For example they can choose to identify validators who systematically approve the same people or who validate their own expense reports. Analyses of the descriptions of these entries can sometimes be very useful. We have found that attempts to conceal fraud are often what make it most obvious to detect.

Stop it; before it starts

Sharing approval processes, and more generally, ensuring a proper segregation of duties whenever there is a cash output, can deter fraud. A sense of impunity is created when processes sit in silos and critical changes depend on a single individual. Strengthening controls and connecting finance, procurement and audit data flows reduces that space, where fraud thrives. With structured workflows, shared visibility and automated monitoring, fraudulent actions become detectable early and therefore far riskier for anyone tempted to act.

It’s time to improve your organisation’s controls and remove isolated decision points, to reduce both the opportunity and the rationalisation that make fraud possible. Don’t let fraud run unnoticed in your organisation for years.

The post When Process Breaks Down, Fraud Finds a Way: Through Invoices, Expenses or Both! appeared first on The Fintech Times.